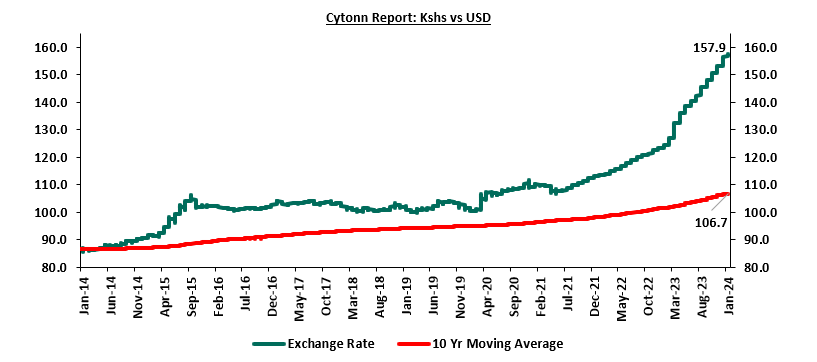

In the first week of the year the Kenyan Shilling experienced a 0.6% depreciation against the US Dollar, closing at Kshs 157.9 as of January 5, 2024, compared to Kshs 156.9 at the beginning of the year. This adds to the 26.8%, 9.0%, and 3.6% depreciation in 2023, 2022, and 2021, respectively. Notably, this is the lowest the Kenyan Shilling has reached against the US Dollar. The ongoing depreciation is primarily fuelled by a stable dollar currency globally after gaining in 2022, a persistent current account deficit, negative trade deficit and lower inflows into the capital markets.

The interest rates have seen significant increases over the last one year with the 91-day treasury bill rates getting to a high of 16.0%. In the Euro bond market, the rates have been high with Euro bonds trading at rates of over 15.0% in December 2023. The high interest rates have increased due to increased demand for cash by government as they continue to run a fiscal deficit and as they seek to get cash to rollover the redemptions. The downgrade by the various rating agencies has worsted the situation. In May 2023, Moody's downgraded Kenya's senior unsecured debt rating, along with its long-term foreign-currency and local-currency issuer ratings, transitioning to B3 from B2. Similarly, Fitch Ratings downgraded Kenya's Long-Term Foreign-Currency Issuer Default Rating (IDR) from 'B+' to 'B' with a Stable Outlook in December 2022;

We have previously covered the topic as summarized below;

- In February 2023, we covered Currency and Interest Rates Outlook-2023, with our outlook on the currency being a 6.4% depreciation mainly on the back of the ever present current account deficit with Kenya being a net importer, which was to increase US Dollar demand in the market, and, the high global crude oil prices that had weighed in on the US Dollar demand from oil and energy importers. On the interest rates, we expected an upward readjustment on the yield curve due to the increased pressure on the government to meet its budget deficit by borrowing more domestically, coupled with Uncertainties about the economy occasioned by elevated inflationary pressures which had resulted in high credit risk hampering lending to businesses and individuals.

- In our Currency Outlook covered in May 2022, our outlook on currency was 4.7% depreciation by the end of 2022 mainly driven by high global oil prices, persistent supply chain bottleneck constraints, and ever present current account deficit,

- In May 2021, we released our topical on Currency and Interest Rates Outlook-2021, with our outlook on currency being a 0.6% appreciation by the end of 2021. The expected appreciation was on account of gradual improvement in the export sector as Kenya’s trading partners continued to reopen their economies coupled with stable forex reserves on the back of increasing diaspora remittance inflows as well as continued investor capital inflows and debt relief from other institutions. On the interest rates, we expected an upward readjustment on the yield curve due to the increased pressure on the government to plunge in the budget deficit coupled with the increased demand by investors for higher yields due to the perceived risk in the country ahead of 2022 general election, and,

- In our Currency and Interest Rates Outlooktopical which was covered in May 2020, our outlook on the currency was a 5.5% depreciation by the end of 2020, driven by the reduced exports earning due to the lockdown measures put in place by Kenya’s trade partners coupled with the high fiscal deficit seen during the period. On the interest rates, we expected a slight upward readjustment on the yield curve due to increased demand by investors for higher yields arising from the perceived risk in the country.

With the shilling having depreciated by 26.8% at the end of 2023 and the continuous upward readjustment on the yield curve, we saw the need to revisit the topic of currency and interest rates outlook, in order to shed some light on how the Kenyan shilling and the interest rates are expected to behave in 2024. In this focus, we shall be doing an in-depth analysis of the factors that are expected to drive the performance of the Kenyan shilling and the interest rates and thereafter give our outlook for 2024 based on these factors. We shall cover the following:

- Historical Performance of the Kenyan Shilling and Drivers,

- Evolution of the Interest Rate Environment,

- Currency Outlook,

- Factors Expected to Drive the Interest Rate Environment, and,

- Conclusion and Our View Going Forward.

Section I: Historical Performance of the Kenyan Shilling

The Kenyan shilling has depreciated at a 10-year CAGR of 6.1% to close at Kshs 157.9 as of 5th January 2024 from Kshs 86.9 over the same period in 2014, Mainly attributable to challenges within the country’s macroeconomic environment. Over the last years we have seen the country run a fiscal deficit that is 8% of GDP which has led to the government borrowing both locally and internationally. The Country has also seen the currency depreciate due to the negative current account deficit currently at 3.5% of GDP. The current account deficit is largely due to the high imports of petroleum products and the manufacturing equipment. In 2023, the shilling depreciated for the sixth consecutive year, closing the year at Kshs 156.5 against the US Dollar as compared to the Kshs 123.4 at the beginning of the year translating to a depreciation of 26.8%. However, the shilling’s steady decline over the past two years could also be seen as a correction from overvalued levels. The chart below illustrates the performance of the Kenyan Shilling against the US Dollar over the last 10 years:

Source: Cytonn Research

The following are the factors that have continued to support the shilling;

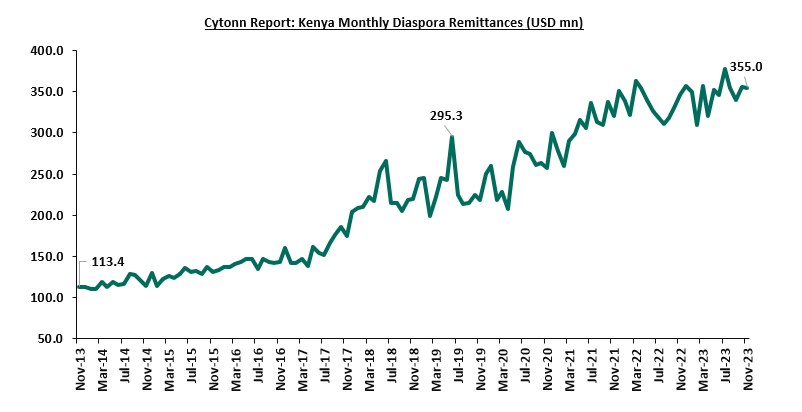

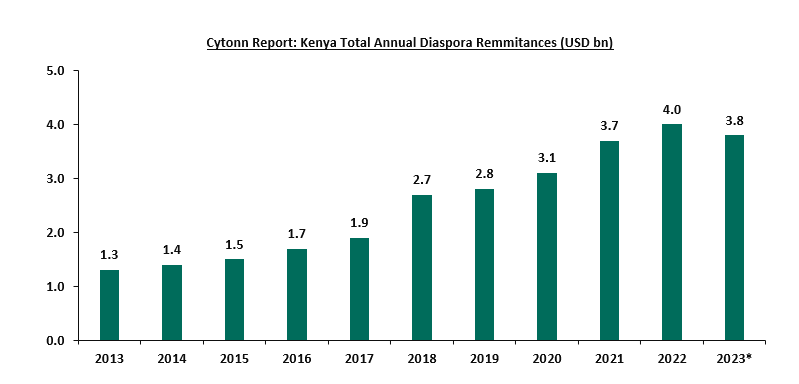

- Strong diaspora remittances, with monthly diaspora remittances having grown at a 10-year CAGR of 12.1% to USD 355.0 mn in November 2023, from USD 113.4 mn recorded in November 2013. In November 2023, the Diaspora remittances stood at a cumulative USD 3,817.4 mn which is 4.0% higher than the USD 3,670.6 mn recorded over the same period in 2022. The continued growth in diaspora remittance is mainly attributable to the recovery of the of the global economy, increasing Kenyan population in the diaspora and advancing technology that has facilitated easier transfer of money. The charts below show the trend of the evolution of monthly and annual Diaspora Remittances;

Source: Central Bank of Kenya

Source: Central Bank of Kenya, * figure as of November 2023

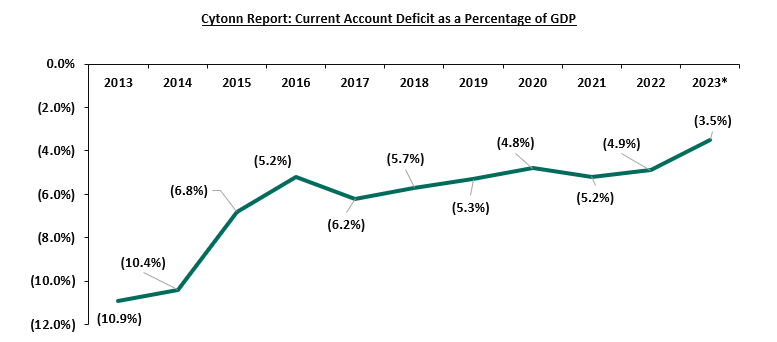

- The narrowing of the current account deficit due to the increased value and volumes of the country’s principal exports. The deficit narrowed to a deficit of 3.5% of the GDP as of Q3’2023, from a deficit of 6.4% recorded in similar period the previous year. Notably, in Q3’2023, the value of tea exports and horticulture contributed Kshs 50.1 mn and Kshs 48.8 mn, respectively out of the total value of exports of Kshs 269.4 mn, which is an increase from a contribution of Kshs 40.2 mn and Kshs 34.6 mn, respectively recorded in a similar period the previous year,

- Kenya has continued to receive financing from the International Monetary Fund and the world Bank which have supported the Kenyan shilling by boosting the forex reserves. Notably, the government received USD 1.0 bn from the World Bank loan under the Development Policy Operation (DPO) facility in May 2023, as well as USD 415.0 mn from the International Monetary Fund (IMF) in July 2023 under the 38-month Extended Fund Facility (EFF) and Extended Credit Facility (ECF) following the completion of the fifth review and is expected to receive USD 682.3 mn upon completion of the sixth review,

- The high Interest rates: The monetary Policy committee increased the Central Bank rate (CBR) to 12.5% signalling a tightening stance to support the shilling and tame inflation. According to the MPC, the increment was made to tame the local currency depreciation, which the Committee noted had a significant contribution to the country’s inflation, contributing 3.0% of the 6.8% inflation rate recorded in November 2023, as well as the high cost of debt service. Interest rates on government securities remain high which are attractive to foreign investors especially the infrastructure bond which is also tax free.

- The Government measures to stabilize the foreign exchange market which include the Government-to-Government petroleum supply arrangement. According to the Draft 2024 Budget policy, this arrangement was mainly intended to address the US Dollar liquidity challenges and exchange rate volatility caused by the global US Dollar shortage and spot market reactions that were driving volatility and causing a false depreciation.

However, the shilling has been put under significant pressure by;

- The existence of an ever-present current account deficit. It is good to note that there has been a positive trend with the Current account deficit coming at 3.5% of GDP in Q3’2023, from the 6.4% recorded in a similar period the previous year and 4.9% of GDP by end of 2022. The ever-present current account deficit reflects the country’s reliance on imports and with the high global commodity prices, it has resulted in increased demand for foreign currency which continue to put more pressure on the local currency. The chart below highlights the trend in the current account deficit as a percentage of GDP for the last 10 years:

Source: Kenya National Bureau of Statistics (KNBS), * figure as of October 2023

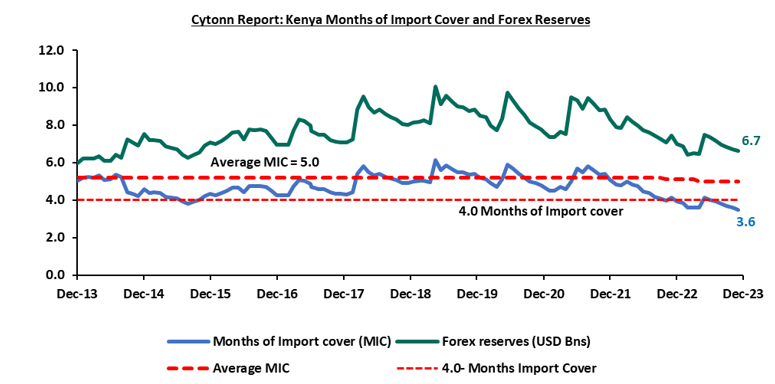

- Dwindling forex reserves having declined by a significant 11.0% to USD 6.7 bn (equivalent to 3.6 months of import cover) in December 2023, from USD 7.5 bn (equivalent to 4.0 months of import cover) in a similar period in 2022. Notably, for the last five months, forex reserves have remained below the statutory requirement of maintaining at least 4.0-months of import cover. The drop is largely attributed to increased debt service obligations due to the continued depreciation of the Kenyan shilling. The chart below shows the trend of the evolution of the forex reserves:

- High global crude oil prices which had been worsened by the supply chain constraints leading to increased demand with fuel being a major input in most sectors in the economy. Consequently, this increased US Dollar demand by oil and energy importers, as well as manufacturers against a low supply of US Dollar currency.

- High debt servicing costs, there are couple of debt maturities happening now a good example is the Eurobond which is meant to be paid by June this year. The cost of paying for the coupons on the Eurobonds has also increased mainly as a result of continued depreciation of the shilling.

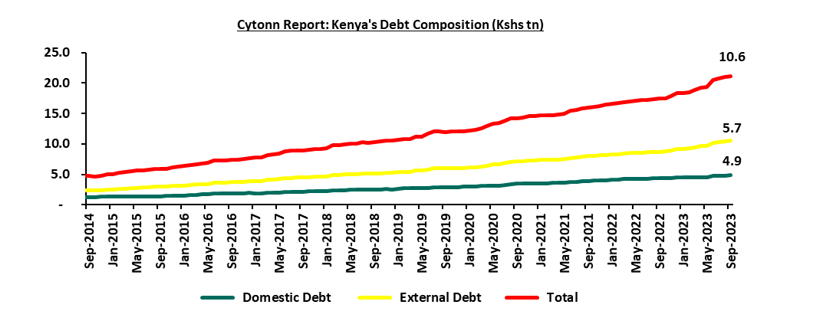

- The high debt levels in the country with the Kenya’s public debt having grown at a 10-year CAGR of 17.8% to Kshs 10.6 tn in September 2023, from Kshs 2.1 tn in September 2013, with external debt accounting for 53.5% of the total debt. This continues to put pressure on our foreign reserves due to the burden of increased debt serving costs and hence continues to weigh down on the Kenyan shilling. The chart below highlights the trend in the country’s debt composition:

Section II: Evolution of the Interest Rate Environment in Kenya

Section II: Evolution of the Interest Rate Environment in Kenya

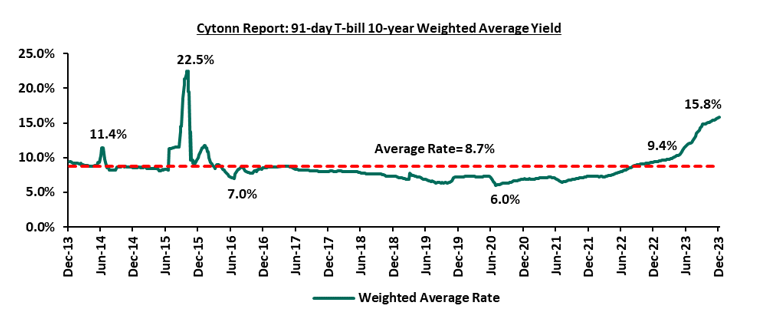

In the FY’2023, interest rates were on an upward trajectory with rates on the 91-day paper rising steadily by a cumulative of 651.4 basis points to close the year at 15.9%, up from the rate of 9.4% recorded at the beginning of the year. The significant increase in interest rates is attributed to the governments increased borrowing needs. In addition, Kenya experienced a deterioration in its credit ratings with Fitch, Moody’s and S&P Global downgrading the country’s outlook from stable to negative following the liquidity challenges and limited access to the international markets amidst the upcoming Eurobond maturity of USD 2.0 bn due in June 2024. The downgrades of Kenya’s credit score have affected the country’s ability to access cheaper loans in the international financial markets, prompting investors in the domestic market to demand higher yields.

Over the last 10-year yields on government papers have remained steady for the most part, with the yields on the 91-day paper averaging 8.7%. However, Kenya’s interest rates witnessed high volatility in the years 2015 and 2016 with the 91-day paper hitting a record high of 22.5% in October 2015 attributed to the tight monetary policy stance adopted by the Central Bank of Kenya, with the Monetary Policy Committee (MPC) raising the CBR to 10.0% in June 2015 from 8.5% in order to anchor inflationary expectations and curtail demand pressures in the economy. In addition to raising the CBR, the MPC also enhanced its open market activities to withdraw excess liquidity from the market. The chart below highlights the trend in the 91-day T-bill weighted average yield for the last 10 years:

The Kenyan macroeconomic environment remains subdued mainly as a result of the elevated inflationary pressures and aggressive depreciation of the Kenyan Shilling that have suppressed business production levels as evidenced by the Purchasing Managers Index (PMI) which averaged 48.1 in the year 2023. As such, we expect revenue collection to lag behind the revised target. The revised budget expenditure stands at Kshs 3,931.4 against revenue collection projection of Kshs 2,894.9 bn for the FY’2023/24.

Our view is that the government should take the following measures to alleviate the strain on the interest rate:

- Focus on domestic borrowing in the short and medium term. The rationale behind this recommendation lies in the cost-effectiveness of domestic debt compared to foreign currency-denominated debts. Domestic borrowing provides the government with a more economical source of debt, considering the higher interest rates and currency risks associated with foreign currency-denominated debts,

- The government should adopt measures to reduce corruption, improve transparency, and strengthen governance structures. A corruption-free environment attracts foreign direct investment, enhance economic efficiency, and instils confidence in the stability of the interest rate environment.

- Shift financing strategies to give priority to concessional financing, while limiting the use of commercial borrowing. This approach will alleviate pressure, especially considering the current depreciation of the shilling. Concessional funding, with its low interest rates and extended repayment periods, is a more sustainable option,

- Continue implementing measures to reduce the debt service-to-revenue ratio, which stood at 58.6% as of November 2023, 28.6% points higher than the recommended threshold of 30.0%, and 1.8% points higher than FY2022/23’s debt service ratio of 56.8%. This increase is mainly due to heightened debt service obligations, largely driven by the depreciating Kenyan Shilling,

- Diversify the funding of projects by removing impediments to Private Public Partnerships (PPPs) and joint ventures. This move aims to attract increased private sector involvement in funding developmental projects, particularly in infrastructure, thereby diminishing the necessity for extensive government borrowing,

- Implement measures that will encourage foreign investment through FDIs, a move that will improve the country's economic standing. A steady inflow of foreign capital contributes to foreign exchange reserves, potentially reducing the need for aggressive domestic borrowing and mitigating pressure on interest rates,

- Contain the government expenditure by limiting expenditure to the core activities of the government as well as eliminating corruption and wasteful spending at both the County and Central government levels, and,

- Maintain overall macroeconomic stability, including controlled inflation rates and a stable exchange rate through policies implemented by the Central Bank in shaping the interest rate environment. Prudent monetary policies and effective management of liquidity contribute to stability and predictability in interest rates and this can instill confidence in investors and lenders, positively impacting interest rates.

Section 4: Currency Outlook

|

Driver |

Outlook |

Effect on the currency |

|

Balance of Payments |

• The deterioration of the country’s balance of payments is likely to put more pressure on the shilling. Notably, Kenya’s balance of payments position (BoP) deteriorated, registering a deficit of Kshs 131.5 bn in Q3’2023, from a deficit of Kshs 112.7 bn recorded in Q3’2022, and a reversal from the Kshs 152.9 bn surplus recorded in Q2’2023. This was caused by a wider deficit in the financial account due to the reduced capital flows following the country’s macroeconomic uncertainties, a trend likely to continue in 2024. As such, we expect a muted foreign direct investment leading to reduced inflows and hence weighing down the shilling. • We expect the country’s reliance on imports coupled with high global commodity prices to continue weighing down on the country’s Balance of payments. As such, with Kenyan being a net importer, we expect to see inflated import bill mainly as a result of the high fuel prices coupled with the continued depreciation of the shilling • However, we expect the gradual improvement in the export sector as Kenya’s trading partners continue to reopen will see the current account narrow as evidenced by the 42.1% narrowing of the current account balance deficit to Kshs 122.5 bn in Q3’2023 from Kshs 211.6 bn in Q3’2022.

|

Negative |

|

Government Debt |

• We expect the government to continue borrowing more domestically as it aims to bridge the fiscal deficit, which is projected to come in at 5.3% of the GDP in the FY’2023/2024. Domestic debt provides the government with a cheaper source of debt compared to foreign currency-denominated debts that have higher interest rates and have currency risk attached to them, • Similarly, external borrowing is expected to increase in 2024 given the need to service the upcoming maturities such as the 10-year USD 2.0 bn (Kshs 226.0 bn) Eurobond maturing in 2024. Notably, Kenya is currently under risk of high debt distress mainly as a results of increasing debt levels, rising debt repayments cost and slow revenue growth with the country’s debt to GDP ratio currently at 70.2%, 20.2% above the recommended IMF threshold of 50.0% for developing countries, • The high debt levels will continue to expose the shilling to exchange rate shocks and will, in turn, emanate pressure on the shilling to weaken during the repayment period. |

Negative |

|

Forex Reserves |

• As of December 2023, the country’s forex reserves stood at USD 6.7 bn (equivalent to 3.6 months of import cover) with the forex reserves having dropped below the statutory requirement of maintaining reserves equivalent to least 4.0-months of import cover, • Notably, the forex reserves have significantly dropped by 11.0% to USD 6.7 bn (equivalent to 3.6 months of import cover) in December 2023, from USD 7.5 bn (equivalent to 4.2 months of import cover) recorded in December 2022. The drop is largely attributed to increased debt service obligations due to the continued depreciation of the Kenyan shilling, • Additionally, the elevated debt levels witnessed in the country are likely to put forex reserves under pressure as most of it will be used to finance the debt maturities, • However, we expect the reserves to be supported by improving diaspora remittance inflows which came in at cumulative USD 3,817.4 mn as of November 2023, 4.0% higher than the USD 3,670.6 mn recorded over the same period in 2022 and the increasing exports especially in the agricultural sector with government having subsidized key inputs such as fertilizers. This will in turn support the stability of the Kenyan Shilling |

Negative |

|

Monetary Policy |

• Inflation rates have remained within the government’s target of 2.5% - 7.5% for six consecutive months despite the high fuel prices in the country following the recent tightening of the monetary policy. Notably, in its latest sitting, the MPC raised the CBR by 200 basis points a move which it termed as aiming to ease the pressure on Kenyan shilling. The impact of this is expected to continue easing inflationary pressures and as such support the shilling • Consequently, we may see slight upward pressure on the interest rates as the ripple effects of the increased CBR continue to reflect in economy in the short to medium term. |

Neutral |

From the above currency drivers, 3 are negative (Balance of payment, Government Debt Forex Reserves), while 1 is neutral (Monetary Policy) indicating a negative outlook for the currency.

Section III: Factors Expected to Drive the Interest Rate Environment

- Monetary Policy

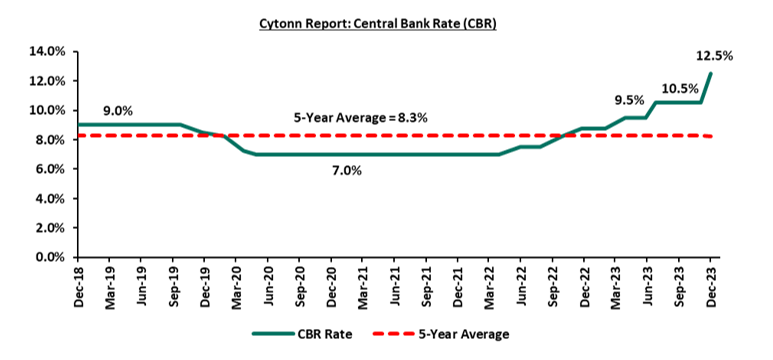

The monetary policy committee has continued to play a crucial role in determining the interest rates levels in the country. In 2023, notable changes in interest rates began in July when short-term government securities were at the rates of 11.9%, 11.9%, and 12.2% for 91-day, 182-day and 364-day papers respectively. This upward trajectory gained momentum following the Central Bank's decision to increase the base lending rate by 100 basis points to 10.5%, from the existed 9.5% and maintained the same rate in its August and October meetings in a move to contain inflation which stood at a high of 7.9% as of June 2023, 0.4% points above the target range of 2.5%-7.5%. In its latest meeting held in December, the MPC raised the CBR further by 200.0 bps to 12.5%. The policy rate influences the cost of borrowing for banks and consequently, affects the rates at which they lend to businesses and individuals. This, in turn, creates a ripple effect on the overall interest rate environment, including the yields on government securities. Since then, the rates for short-term government papers have soared, reaching 15.9%, 16.0%, and 16.1% for 91-day, 182-day, and 364-day papers, respectively as of December 2023. The Central Bank is expected to continue with the restrictive monetary policy stance in the medium term with the intention to maintain inflation within CBK’s target range of 2.5%-7.5%. As such, we expect to see continued upward pressure on the interest rates as the government compensates investors for the increased risks posed by currency depreciation and elevated inflation. The following is a graph highlighting the Central Bank Rate for the last 5 years;

- Fiscal policies

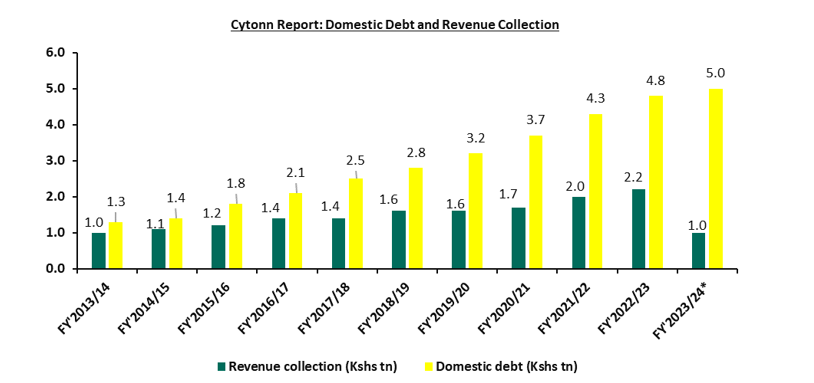

The government continues to put in place measures to broaden the revenue base and rationalize expenditures in order to reduce the fiscal deficits. In June 2023, the National Treasury presented Kenya’s FY’2023/24 National Budget to the National Assembly highlighting that the total budget estimate for the 2023/24 fiscal year increased by 8.7% to Kshs 3.7 tn from the Kshs 3.4 tn in FY’2022/23 budget. According to the Draft 2024 Budget Policy, the budget execution during the first four months of FY’2023/24 progressed relatively well with revenues recording a growth of 13.0% in October 2023 compared to a growth of 11.9% in October 2022. The FY’2023/24 budget focuses mainly on providing solutions to the heightened concerns on the high cost of living, the measures put in to accelerate economic recovery as well as undertaking a growth-friendly fiscal consolidation to preserve the country’s debt sustainability. Notably, the government projects to narrow the fiscal deficit to 5.4% of GDP in FY’2023/24, from the estimate of 5.8% of GDP in FY’2022/23. However, the upward revision of taxes comes at a time when the business environment remains subdued, underpinned by the elevated inflationary pressures and the aggressive depreciation of the Kenyan shilling that has suppressed business production levels weighing down on the projected revenue performance. As such, we expect this will significantly affect revenue collection necessitating borrowing to plug in the budget deficit. Below is a chart showing the revenue collections and domestic borrowings over the last 10 financial years:

- Liquidity

The MPC lowered the Cash Reserve Ratio (CRR) to 4.25% from 5.25% in their March 2020 sitting, which has since remained unchanged aimed at supporting the economic recovery from the ripple effects of Coronavirus pandemic. As a result, liquidity in the money market has remained relatively favourable as evidenced by the interbank rates at an average of 9.8% in 2023, compared to an average of 4.9% in 2022, with average interbank volumes increasing by 16.1% to Kshs 21.6 bn in 2023, from Kshs 18.6 bn in 2022. In an ideal situation, ample liquidity in the money market, the lowering of commercial banks’ lending, and deposit rates would lead to increased money supply in the economy and an increase in consumers’ purchasing power. The low Cash Reserve Ratio has played a big role in maintaining favourable liquidity in the money market as well increases the supply of money by commercial banks. We expect liquidity to improve in 2024 driven by increased access to credit as banks gradually increase their lending to the private sector and the continued adoption of risk-based lending by banks. However, due to uncertainties in the economy occasioned by elevated inflationary pressures, there still exists a high credit risk which hampers lending to businesses and individuals.

Outlook:

|

Driver |

Outlook |

Effect on Interest Rates |

|

Fiscal Policies |

• The government is expected to continue borrowing in order to offset the budget deficit and finance debt maturities. The total T-bonds and T-bill maturities so far stand at Kshs 161.7 bn and Kshs 462.2 bn, respectively for the year 2024 which will in turn put pressure on rates |

Negative |

|

Monetary Policy |

• We expect the MPC to continue with the tightening of the monetary policy in the short term in a bid to stabilize inflation within the government’s target and anchor the Shilling from further depreciation. This is evidenced by the recent actions taken by the MPC where it increased the CBR by 200 basis points to 12.5% from 10.5%. • As such, the yields on government securities are likely to adjust further upwards as investors attach a higher premium to meet their required real rate of return, |

Neutral |

|

Liquidity |

• We expect liquidity to continue being supported by the Low Cash Reserve Ratio (CRR) currently at 4.25% from 5.25% previously. • Additionally, we expect liquidity to improve in 2023 driven by increased access to credit as banks gradually increase their lending to the private sector and the continued adoption of risk-based lending by banks. This will in turn push up the interest rates due to increased competition between the private sector and the government. • The huge maturities from government securities are expected to increase liquidity |

Neutral |

From the above indicators, 1 of the drivers is negative (fiscal policies), and 2 are neutral (Monetary policies and liquidity). We therefore believe that the interest rate environment remains uncertain and will likely adjust upwards.

Section IV: Conclusion and Our View Going Forward

Based on the factors discussed above and factoring in the uncertainties in the Kenyan macroeconomic environment;

- We expect the Kenya Shilling to trade within the range of between Kshs 183.2 and Kshs 189.6 against the USD by the end of 2024 based on the purchasing power parity (PPP) and interest rate parity (IRP) approach respectively, with a bias of a 16.4% depreciation mainly driven by:

- The persistent US Dollar demand by importers, mainly in the oil and energy sector as well as manufacturers, while the US Dollar supply remains low resulting to a shortage of USD in the Kenyan market,

- The ever present current account deficit with Kenya being a net importer, which will increase US Dollar demand in the market,

- The deteriorating forex reserves which have for the last five months remained below the statutory requirement of maintaining at least 4.0-months of import cover. The drop is largely attributed to increased debt service obligations due to the continued depreciation of the Kenyan shilling, and,

- A continued hike in the US Federal interest rates, with the Fed raising the rates by 100 bps in July 2023 to a current range of 5.25%-5.50% from a range of 4.25%-4.50% in December 2022. The hike in rates, meant to curb inflation in the US has strengthened the US Dollar against other currencies resulting in capital outflows from emerging and developing markets such as Kenya.

- We expect a continued upward readjustment on the yield curve with our sentiments being on the back of:

- The government faces mounting pressure to address its budget deficit by increasing its domestic borrowing. The government is likely to continue accepting expensive bids and in turn continue destabilizing the interest rate environment, and,

- Uncertainties about the economy occasioned by elevated inflationary pressures which have resulted in high credit risk which hampers lending to businesses and individuals. Additionally, with the approaching USD 2.0 bn Eurobond maturity in June 2024 will likely push the yield curve upwards as investors attach high attaching higher yields due to the uncertainty on the government repayment.

Concerns persist regarding the future performance of the Kenyan shilling, fuelled by existing pressures, dwindling foreign exchange reserves and escalating levels of national debt with the approaching maturity of the USD 2.O Eurobond in June 2024. Anticipating a continued depreciation of the currency, we foresee adverse consequences in the economy, marked by an augmented import bill. Despite the implementation of a tightened monetary policy, with MPC increasing the rate to 12.5% in December 2023 from 10.5%, short-term inflation is expected to remain elevated, mainly because inflation in the country is mainly cost driven rather than demand driven, as the money supply remain stable. Although the current strain on the Kenyan shilling is unlikely to ease in the immediate future, there are proactive measures that the government can adopt to alleviate further depreciation. These measures encompass strategic interventions and policies aimed at stabilizing the currency and fostering economic resilience. They include:

- Formulate policies to encourage Foreign Direct Investments (FDIs): The government should prioritize creating an attractive investment environment for foreign investments by improving transparency in all required regulations as well as reducing hurdles in the process. This would include targeting sectors that enjoy global interest like the Renewable Energy sector and Sustainable Energy Development Goals (SEDG), and could include incentives for the same. This would majorly increase the foreign exchange reserves thus reducing the pressure on the foreign currency in the Kenyan markets,

- Promotion of Tourism through Implementing robust marketing campaigns to attract international tourists and enhancing the tourism infrastructure which will help increase the inflow of dollars and hence boost our Foreign Exchange Reserves

- Dramatically cut Spending: The government should Contain expenditure by limiting expenditure to the core activities of the government as well as reducing wasteful spending at both the County and Central government levels

- Reduce corruption: The government should adopt measures to reduce corruption, improve transparency, and strengthen governance structures. A corruption-free environment attracts foreign direct investment, enhance economic efficiency, and instils confidence in the stability of the Kenyan Shilling.

- Stimulate our moribund capital markets to attract foreign investors: The government should focus on improving the capital markets by Implementing policies that encourage foreign investment, streamlining regulatory frameworks, and introducing investor-friendly initiatives. A vibrant capital market attracts foreign capital as well as enhances liquidity and diversifies investment options, contributing positively to currency stability.

- Maintaining a sustainable debt level: The government should find a harmonious equilibrium between engaging in foreign borrowing to boost foreign reserves and preserving a favourable credit standing with creditors. This delicate balance is crucial for maintaining the country's attractiveness to investors, facilitating capital inflows and financial stability. Consequently, the government should be proactive in meeting upcoming financial obligations, such as the impending USD 2.0 bn Eurobond maturing in June 2024,

- Reduction of commercial loans: There is need for the government to reduce the share of commercial loans in order to reduce debt servicing costs. This is mainly because commercial loans attract higher interest rates as compared to concessional borrowings. Reduced debt service amounts would greatly help to bring down demand for the US Dollar and stabilize the exchange rate,

- Building an export-driven economy: The government can do this by formulating and implementing robust export-oriented policies and manufacturing to increase exports aimed at reducing the current account while reducing overreliance on imports to preserve the country’s foreign exchange reserves,

- Alternative projects financing strategies: The government should diversify the sourcing of funding for infrastructure projects in the country to further shift to alternative financing strategies such as Public-Private Partnerships (PPPs), joint ventures and stimulation of the capital markets. This will attract more private sector involvement in funding development projects such as infrastructure instead of borrowing, and,

- Formulation of diaspora-friendly policies: The Government should work in close conjunction with banks and other investment institutions to allow for favourable accounts for diaspora citizens, which will encourage them to remit more money back to the country hence cushioning the shilling against further depreciation. This can be done by reducing money transfer costs by exploring alternative channels for remitting money by leveraging on digitization and technology and explore alternative channels,

- Improve Ease of Doing Business: Improving the ease of doing business will make it easier for entrepreneurs to form business ventures, which will eventually grow, employ people and contribute to tax revenues, and,

- Encourage export and revenue diversification: the government should shift from complete over-reliance on traditional agricultural sector exports like tea, horticulture and coffee, through diversification in promoting value-added processing and manufacturing to increase export revenue. Notably, the manufacturing sector contribution to GDP remains low, coming in at only 8.3% in Q3’2023, hence the government should put in policies to grow the sector like incentives which would in turn increase exports as well as preserving the foreign exchange reserves, aiding in stabilizing the exchange rate.

Disclaimer: The views expressed in this publication are those of the writers where particulars are not warranted. This publication, which is in compliance with Section 2 of the Capital Markets Authority Act Cap 485A, is meant for general information only and is not a warranty, representation, advice or solicitation of any nature. Readers are advised in all circumstances to seek the advice of a registered investment advisor.