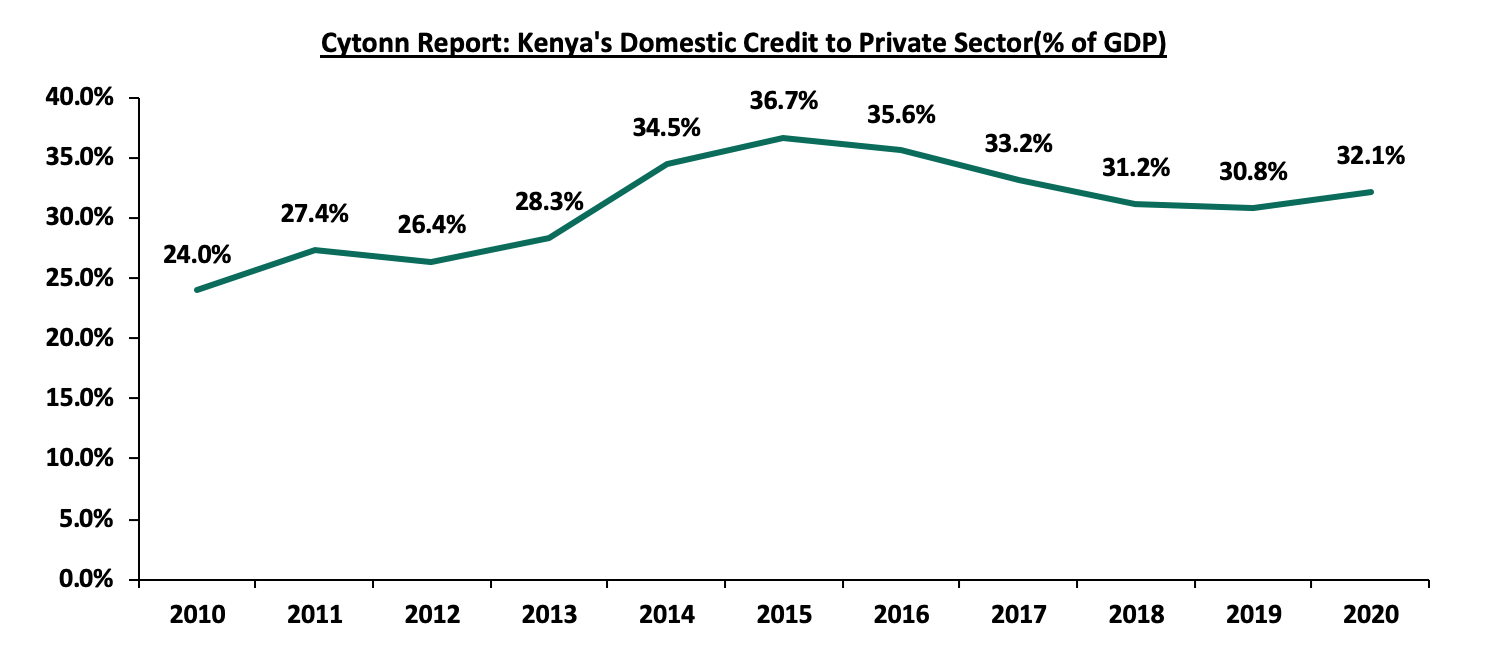

As highlighted in our topical on Private Sector Credit Growth, Kenya’s domestic credit extended to private sector as a percentage of GDP was at 32.1% in 2020, compared to the 38.9% average for the Sub-Saharan African region, 111.2% for South Africa and 164.2% for advanced economies, highlighting the gap in credit availability for businesses. To achieve 100.0% Private Sector Credit to GDP, Kenya needs total credit to private sector of Kshs 12.1 tn, current credit to private sector is Kshs 3.4 tn, hence the current Kshs 8.7 tn deficit in credit to the private sector. The Hustler fund, if sustainable, at Kshs 50.0 bn, would only resolve 0.6% of the problem. The graph below shows domestic credit extended to the private sector over the years;

Source: World Bank

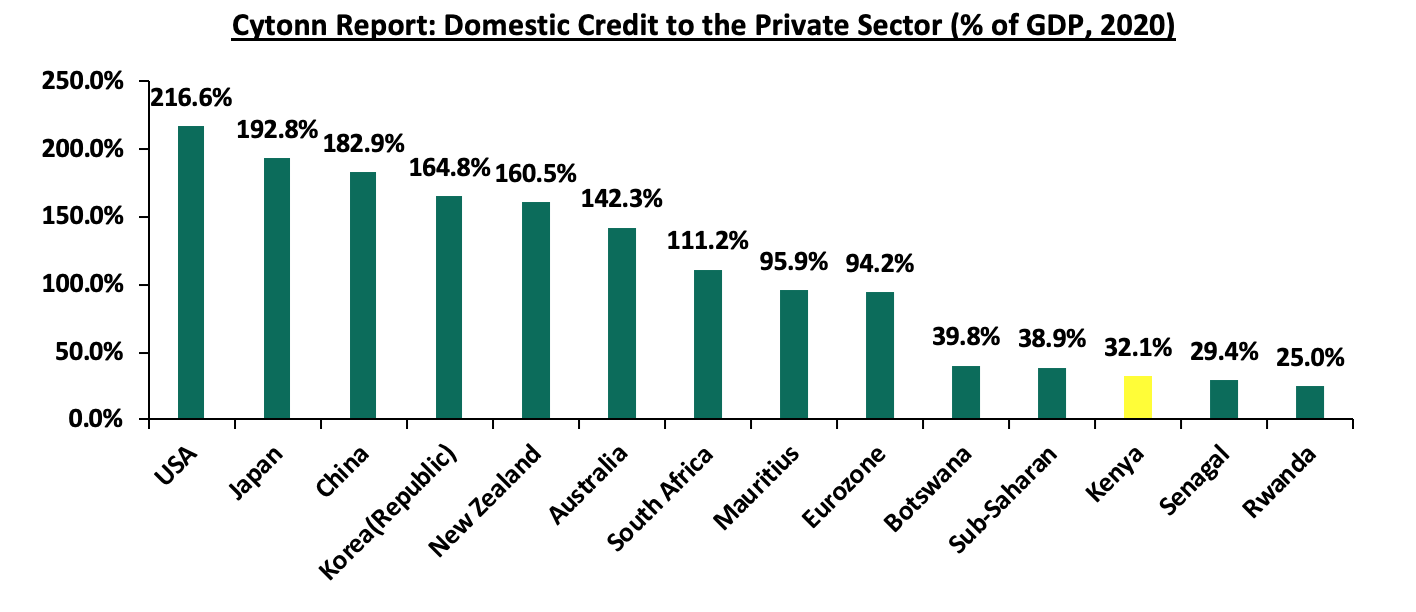

In 2020, Kenya’s Private Sector Credit growth at 32.1% of the GDP was outperformed when compared to advanced economies such as the United States of America and Japan at 216.6% and 192.8%, respectively, as well as Sub-Saharan economies such as South Africa and Mauritius at 111.2% and 95.9%, respectively. The graph below shows the comparison of Kenya’s domestic credit extended to the private sector as a % of Gross Domestic Product (GDP) in 2020 against other select economies;

Source: World Bank

One of the key inhibitors to credit growth has been the failure of our capital markets. In well-functioning markets, credit comes from both banking markets and capital markets with banking markets providing 40.0% of credit and capital markets (both regulated and unregulated) providing the majority balance of 60%. However, in Kenya banks provide 99.0% of credit, essentially, the 32.0% private sector credit to GDP in Kenya all comes from banking markets with no participation from capital markets. Key to note, individuals at the bottom of economic pyramid have suffered more in terms of access to credit mainly because of bureaucratic measures and need for collateral when borrowing from banks coupled with the high interest rates charged. When credit has been advanced by digital credit providers, it has been equally as expensive, with often punitive terms.

In a bid to address the credit gap and in line with pre-election promises, the new administration launched the Financial Inclusion Fund (Hustler Fund) on 30th November 2022, with the fund’s main objective being to improve the credit access to citizens at the bottom of the pyramid who have often struggled to obtain affordable credit. Key to note, the previous governments had introduced various special funds such as Uwezo Fund, Women Enterprise Fund and Youth Enterprise Development Fund in a bid to increase credit access to various target groups. However, success of these funds has been crippled by low recovery rates on advanced amounts, with the recovery rate for the funds at 52.2% and 35.8% for Youth Enterprise Development Fund and Uwezo Fund, respectively. Only the Women Enterprise Fund has recorded a relatively high recovery rate, at 93.3%. Given the first component of the Hustler Fund, the personal finance loan is up and running, this week we turn our focus to the Hustler Fund to have a deeper understanding of the fund by looking at the progress it has made, potential impact, and its sustainability. We shall undertake this by looking into the following;

- Introduction,

- Performance of historical Government Special Funds,

- Structure and Features of Hustler Fund,

- Potential Impact of the Hustler Fund,

- Sustainability of Hustler Fund,

- Recommendations

Section 1: Introduction

The Financial Inclusion Fund, commonly known as Hustler Fund, is a government special sponsored Fund targeting Kenyans of low income to access credit conveniently through their phones. In line with its campaign promise, the new regime launched the fund on 30th November 2022 with a start-up capital amounting to Kshs 50.0 bn. The main objective of the fund is to make credit affordable to majority of citizens who have been out of the formal credit cycle for a long duration. As such, the Fund will lend to all eligible persons at a rate of 8.0% per annum, representing the lowest interest rate in the country. Besides access to credit by people at the bottom of economic pyramid, the fund also aims to promote a savings culture by apportioning 5.0% of the borrowed amount to a savings account where 30.0% will be accessible 365 days after loan disbursement, and 70.0% will be accessible upon retirement. Notably, the fund comprises of four products, that is, Personal Finance, Micro Loan, (Small and Medium Enterprises (SMEs) Loan and Start Ups loan. The Personal Finance component was launched on 30th November 2022 and will offer amounts between Kshs 500 to Kshs 50,000 at a rate of 8.0%. The government also announced plans to launch the SMEs loan with an upper limit of Kshs 2.5 mn in March 2023. The fund is easy to access, and is leveraging on the high mobile penetration in Kenya of 132.5% in 2022 through the collaboration by telecommunication firms in Kenya such as Safaricom, Airtel and Telkom. To apply, citizens can dial a USSD code *254#. According to Co-operatives and MSME Development Ministry, the latest data on total amount borrowed from the fund stood at Kshs 10.1 bn of which Kshs 3.2 bn had already been repaid. The fund’s repayment rate by 16th December 2022 averaged 53.2%. The main objectives of the fund are;

- Promote Financial Inclusion – The fund shall promote financial inclusion through expansion of access to credit by persons, proprietors, MSMEs, SACCOs, and start-ups for economic growth and job creation,

- Ensure Responsible Lending Culture – The fund aims at addressing qualitative dimension of financial inclusion by ensuring responsible lending and borrowing, ethical practises, offering financial literacy and promoting consumer rights,

- Promote Affordable Credit - Come up with market interventions to enhance supply of affordable credit to MSMEs including credit worthiness based lending, risk pricing, business and financial management skills and cost of doing business, and,

- Enhance Health Coverage and Social Security - Improve the low participation of the non-formal wage workforce in health insurance and retirement benefit schemes to ensure universal health coverage and universal social security

Section 2: Performance of Historical Government Special Funds

In Kenya, Special Interest Groups (SIG) Enterprise Funds refer to fund allocation initiatives by the Government of Kenya aimed at improving economic equality and financial inclusion targeting the youth, women and people with disabilities (PWDs). Previous regimes have rolled out three main avenues targeting SIGs which include; Uwezo Fund, Women Enterprise Fund, and Youth Enterprise Development Funds. Below is a summary of the performance of the existing special funds;

- Uwezo Fund - Founded under the Legal Notice No. 21 under the Public Finance Management Regulations in September 2013 to enable women, youth and persons with disabilities to access finance and promote enterprises at the constituency level. Since inception to June 2021, the fund has disbursed a total of Kshs 6.9 bn to 74,884 groups comprising of 47,720 women groups, 25,264 youth groups, and 1900 PWD groups, resulting in an average loan size of Kshs 92,142.5. The fund’s cumulative repayment in the period under review stood at Kshs 2.4 bn, equivalent to a 35.8% repayment rate against a corresponding default rate of 64.2%. The allocation for the Uwezo Fund will be determined under the National Government Affirmative-Action Fund (NGAAF) which has a Kshs 2.1 bn budgetary allocation,

- Women Enterprise Fund – Established under the Legal Notice No. 147 of 2007, the fund has disbursed a cumulative loan amounting to Kshs 21.6 bn to 120,624 self-help groups and 1,882,252 individuals since inception, resulting in an average loan size of Kshs 10,784.5. Key to note in the FY’2020/2021, the fund disbursed Kshs 3.0 bn to 11,361 self-help groups and recovered Kshs 2.8 bn in the period, translating to 93.3% repayment rate against a corresponding default rate of 6.7%. Furthermore, the fund has cumulatively trained 1,516,822 women on entrepreneurship and supported 40,298 women by providing market access and linkages. The government has also allocated Kshs 170.0 mn for the Fund in FY’2022/2023, and,

- Youth Enterprise Development Fund (YEDF) – The YEDF was founded in May 2007 by the Legal Notice No. 63, under the Ministry of ICT, Innovation, and Youth Affairs. Since inception to June 2020, the fund had advanced loans amounting to 12.8 bn to 1,159,393 youths with the average loan size coming in at Kshs 11,040.3 Key to note, Kshs 5.6 bn of the total loan disbursed was directly from the fund itself and the remainder disbursed through financial intermediaries (FI). For FY’2019 /2020, the fund disbursed Kshs 473.3 mn and recovered Kshs 247.2 mn, translating to a repayment rate of 52.2% and a corresponding default rate of 47.8%. Additionally, the fund has facilitated and trained 460,000 youth on entrepreneurial skills, supported 8,191 youths to market their products in trade fairs and helped 28,250 youths get employment opportunities abroad. The government has allocated Kshs 175.0 mn for the FY’2022/2023.

Below is a table showing the funds’ performances:

|

Cytonn Report: Special Interest Groups Enterprise Funds Performance |

|||||

|

Fund |

Amount Disbursed |

Amount Recovered |

Amount Pending Recovery |

Recovery Rate |

Default Rate |

|

Uwezo Fund |

6.7 |

2.4 |

4.3 |

35.8% |

64.2% |

|

Women Enterprise Fund |

3.0 |

2.8 |

0.2 |

93.3% |

6.7% |

|

Youth Enterprise Fund |

0.5 |

0.2 |

0.2 |

52.2% |

47.8% |

|

Average Rates |

60.4% |

39.6% |

|||

*The performance of Uwezo Fund has been taken cumulatively since its inception to the period ending June 2021 while the performances for the Women Enterprise Fund and the Youth Enterprise Development Fund have been taken as per the last financial year of reporting.

**Amounts are in Kshs bn

Section 3: Structure and Features of Hustler Fund

As aforementioned, Hustler Fund has been established to realize the economic model of the new regime by offering credit line to individuals at the bottom of the economic pyramid. Key to note, the government, through the Cabinet Secretary for the National Treasury and Economic Planning tabled the PFM-Financial Inclusion Fund Regulation, 2022 as a guideline towards the operations of the Hustler Fund. The draft regulation provides information on the eligibility to qualify for the fund, the management structure and features of the fund as discussed below;

- Eligibility Criteria

The government has removed many of the administrative bottlenecks when applying for the fund by collaborating with already established telecom and bank platforms such as Safaricom, Airtel and Telkom and KCB bank and Family bank. However, it is important to note that for one to borrow, he/she must meet the prerequisites as stipulated below;

- Natural Person – For a natural person, that is, an individual and not an entity, the applicant shall be eighteen years of age and above and a holder of Kenyan national identity card and satisfy any other requirements that may be deemed necessary by the Board, and,

- MSMEs, SACCO Societies, Chama, Group, table banking group or any relevant association – The applicant within these categories should have all members aged eighteen and above, be registered by the appropriate government institution and comply with any set obligation as may be determined by the Board.

Additionally, an applicant must have a registered mobile number from a recognized mobile operator in Kenya and have mobile money account such as M-pesa, Airtel Money or T-Kash. The sim card to be used during the loan application must have been active for more than 90 days. Importantly, no collateral is required for the loan.

- Governance and Management of the Hustler Fund

The fund shall be managed by a board headed by a non-executive chairperson appointed by the President and shall perform oversight role and further help in formulation of new policies. The board shall consist of;

|

Cytonn Report: Hustler Fund Board Membership |

|

|

1 |

Chairperson (Non-Executive) |

|

2 |

Principal Secretary to the National Treasury or Representative |

|

3 |

The Principal Secretary of the State Department of Trade or his representative |

|

4 |

The Principal Secretary of the State Department for MSMEs or his representative |

|

5 |

The Attorney-General or his representative, |

|

6 |

Two non-public officers appointed by the Cabinet Secretary MSMEs |

|

7 |

Fund Administrator-Ex-officio member (Secretary to the board) |

Source: State Department of Trade

Key to note, the chairperson and all members shall serve for a term of three years and can be appointed for another one term depending on their performance. Additionally, the Fund shall have a Chief Executive Officer who will be competitively appointed by Cabinet Secretary to MSMEs upon recommendations by the board and meeting the relevant requirements. Given that appointees to the Hustler Fund board are either directly appointed by the president of his appointees, such as the CS MSMEs, it can be concluded that the fund is effectively wholly under the direct control of the Office of the President.

- Features of the Hustler Fund

The hustler fund principal loan structure for the Personal Finance product ranges between Kshs 500 - Kshs 50,000 and an individual will only be eligible upon meeting the conditions stated above. According to the Terms and Conditions of the Fund, the term of the loan shall be 14 days with interest charged at annual rate of 8.0% which shall be accrued daily until the full repayment of the loan amount and shall be advanced through the relevant Mobile Money Wallets.

Upon approval of the loan requested by an individual, the loan product shall have a savings component as discussed below;

- Savings Deduction - The fund will deduct 5.0% of the loan advanced that shall go towards savings,

- Short Term Savings – Key to note, 30.0% of the 5.0% savings deduction shall be applied to savings account which will be available to borrowers after 365 days from the disbursement date unless there is a default upon which the borrower can access the funds earlier,

- Pension Remittance – Notably, 70.0% of the 5.0% savings deduction shall be applied towards the customer pension that will be accessible to the borrower upon attainment of the prerequisite age, and,

- Government Contributions – Additionally, the Government of Kenya shall match the Pensions Remittance of a borrower who has not defaulted at a ratio of 2:1. Here, for every Kshs 2.0 saved, the government shall add Kshs 1.0 to a maximum government contribution of Kshs 6,000.0 annually.

Notably, the Hustler Fund has come up with the following precautionary measures to minimize the default rate;

- If the customer fails to pay within the 14 days from the date of disbursement, the loan will attract a higher interest of 9.5% annually with effect from the 15th If the customer further fails to repay by the 30th day from the disbursement date, the bank will review the customer’s credit rating thus affecting the assigned credit limit. Key to note, the interest rate shall apply daily from the date of loan disbursement for a year, or such earlier date when the repayment shall have been completed,

- In case the customer fails to repay the loan by the 30th day from the date of disbursement, he/she will not be eligible to borrow until the repayment of all outstanding debt obligations,

- Further, the fund shall retain 30.0% meant for short term savings in suspense account until full repayment of the loan to mitigate against the risk of total default by borrowers, and,

- Once the customer has settled the outstanding debt, he/she shall have access to amount in the suspended account and will be at liberty to withdraw or keep in savings account.

Section 4: Impact of the Fund

- Potential Impact of Hustler Fund

The Launch of the Hustler Fund Personal Finance Product is commendable and is set to impact Kenyans who are in the bottom pyramid of the economic status by ensuring access to credit at an affordable rate. Key to note, the fund was just recently launched and it is still early to analyze its impact. However, we shall look into the potential impact that the hustler fund will have if it is implemented based on the set objectives. The potential impacts include;

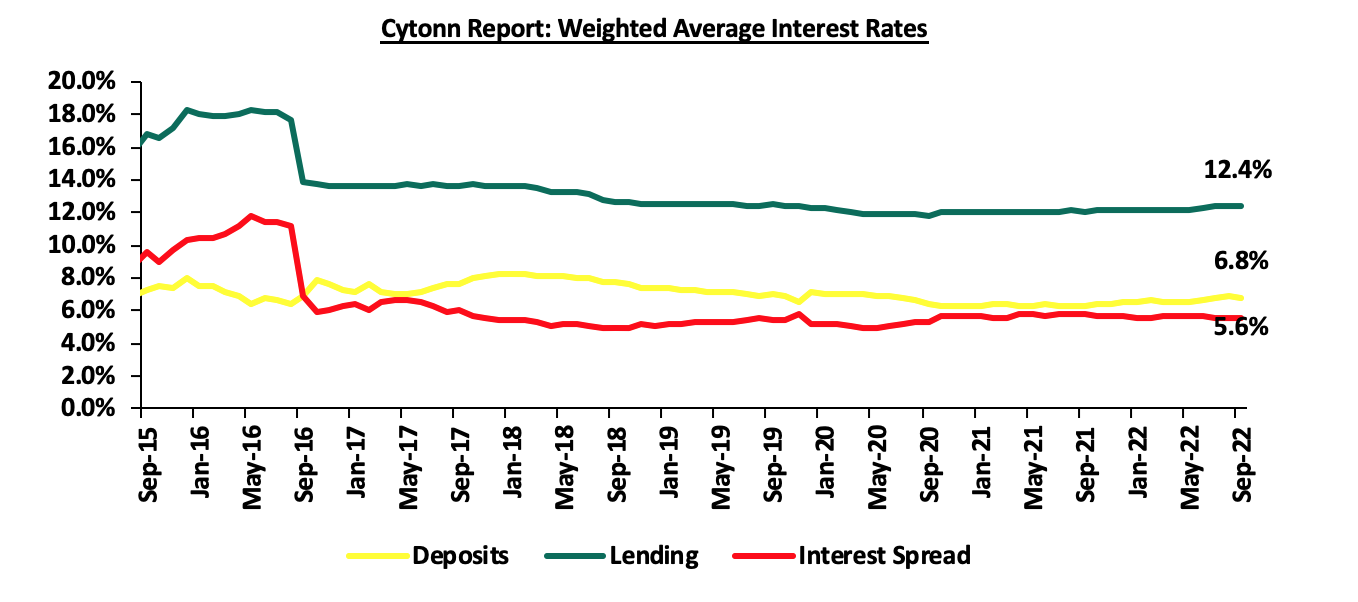

- Access to Cheaper Credit – As highlighted, banks provide 99.0% of credit to businesses in Kenya and is typically very expensive, evidenced by the average lending rate of 12.4% as of September 2022. Additionally, the approval of the Risk-Based Pricing Models for Commercial banks is set to edge the rates higher. Further, the digital loans offered are quite exorbitant leading to CRB listing of many Kenyans, which the government is trying to repair through regulation of digital lenders and the credit repair framework. As such, the 8.0% annual interest rate offered by the fund is cost-effective especially to the target group. Below is a chart showing the Kenya’s weighted average interest rates over the last 7 years;

Source: CBK

- Convenient Access to Loans – The government has made access to Hustler Fund easy through collaboration with the three major telephone companies such as Telkom, Airtel and Safaricom through mobile wallets. This is important as it will reduce the cost of credit when borrowing from banks or other digital lenders operating in the Kenyan market. Application for credit by other lenders involves a lot of bureaucracies and this has been minimized,

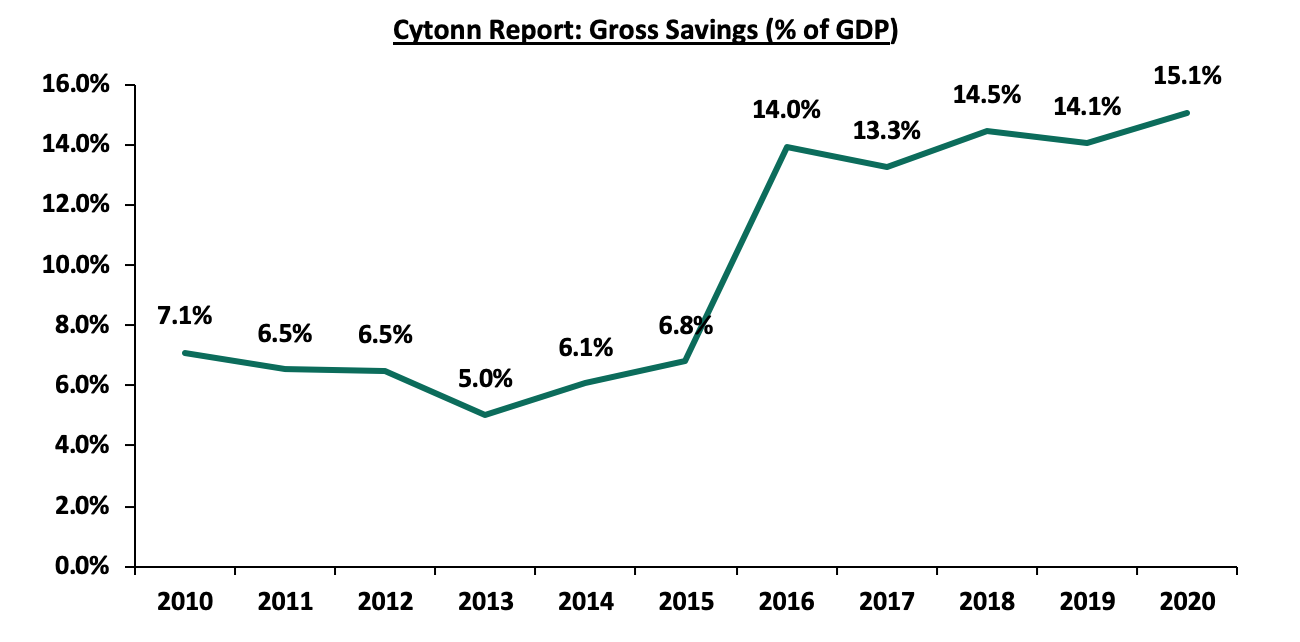

- Improving Savings Culture, Investment and Social Security to Vulnerable Members of the Society – The fund aims to improve the savings culture and investment in social security for Kenyans especially those within the informal sector. As at 19th December 2022, the total amount saved from the fund was Kshs 479.0 mn from Kshs 9.6 bn representing 5.0% of the amount disbursed. According to World Bank, Kenya’s gross saving as a percentage of GDP as of 2020 was 15.0% compared to an average of 23.0% for Sub-Saharan African region indicating the low savings culture in Kenya. As such, the 5.0% savings from Hustler Fund coupled with increasing awareness on the importance of savings will enhance savings culture in Kenya. Below is a chart showing Gross savings as a percentage of GDP in Kenya;

Source: World Bank

- Improving Economic Growth – Key to note, MSMEs contributes almost 40.0% of the GDP indicating the critical role played by this cadre in improving the economy of a country. As such, the fund will widen the access to credit especially in the informal sector consequently improving the economy in the long run.

- Expected challenges and bottlenecks

Kenya has various affirmative action schemes listed above which have been operating for some time. The funds have faced various challenges hence failure to meet their specific objectives. We expect the Hustler Fund, being a special fund to be faced by various challenges that the previous funds have grappled with, including;

- High Default Rate – The fund is likely to suffer from high default rate mainly attributable to tough economic times and unfavorable business environment. The fund’s current average repayment rate is 53.2%, having disbursed Kshs 10.1 bn and received repayments amounting to Kshs 3.2 bn, indicating a 46.8% default rate; the average default rate for the existing affirmative action funds is 39.7% indicating a potential challenge since the fund has not effectively addressed the legal mechanisms to enhance loan recovery,

- Low Loan Limits – Majority of the customers are receiving low loan limits because of the poor credit scores, by participating banks, especially those at the bottom of economic cadre. Additionally, based on the fund’s lending amounts, it is possible for the fund to be used for personal expenses rather than economic benefit which would expose it to high default rates. As such, this defy the logic of the fund since the amounts borrowed are insufficient to empower majority of the beneficiaries to start or expand businesses,

- Corruption and Mismanagement – Historically, government Affirmative Action Funds have been marred with corruption and mismanagement mainly arising from political interference. The auditor general raised questions on the accuracy of the FY’2021/2022 Uwezo Fund Financial Report with cash amounting to Kshs 7.1 bn not being able to be confirmed or reconciled. Similarly, the auditor general also raised queries on estimated Kshs 7.2 bn for the FY’2019/2020 Youth Enterprise Development Fund that could not be confirmed with the relevant documentation. Additionally, an estimated Kshs 3.7 bn from Women Enterprise Fund FY’2021/2022 Report could not be accounted for and there was also irregular procurement of motor vehicle parts. Key to note, Hustler Fund is not immune to this since the members of the board and the management structure are appointed based on political influence, and are all effectively under the control of the Office of the President hence the governance framework is lacking checks and balances. The fund is thus likely to suffer from lack of transparency unless the structures in place to mitigate such circumstances are faithfully implemented. However, its notable that digitization of the fund has reduced human interference

- Lack of Financial Literacy – Majority of the fund’s beneficiaries need financial literacy on dynamics of the growing business environment and how to run small business ventures. Notably, the government has failed on this and may result to misuse and mismanagement of the borrowed funds leading to high default rate rendering the fund unsustainable in the long run,

- High Cost of Operations – According to the draft regulations, the government has capped the cost of operations of the fund at 3.0% of the approved budget. However, failure to properly implement this policy can result to high cost of operations eating on the funds available for borrowing, and,

- Lack of Legal Framework to Recover Funds – The fund has no legal framework upon which to prosecute defaulters and fully recover the money. Additionally, the loan has no collateral and the potential high default rate may lead to unsustainability of the fund in future.

Section 5: Sustainability Analysis of the Hustler Fund

Since its inception, Hustler Fund has disbursed more than Kshs 10.1 bn as at 20th December 2022. The table below details the data on the fund’s transactions as reported by Cabinet Secretary to the Co-operatives and MSME Development Ministry;

|

Cytonn Report: Hustler Fund Transactions Data as of 20th Dec 2022 |

|

|

Amount Disbursed |

Kshs 10.1 bn |

|

Repayment Amount |

Kshs 3.2 bn |

|

Savings Amount |

Kshs 0.5 bn |

|

Total Transactions |

17.5 mn |

|

Opted in Customers |

16.8 mn |

|

Repeat Customers |

3.1 mn |

Source: Co-operatives and MSME Development Ministry

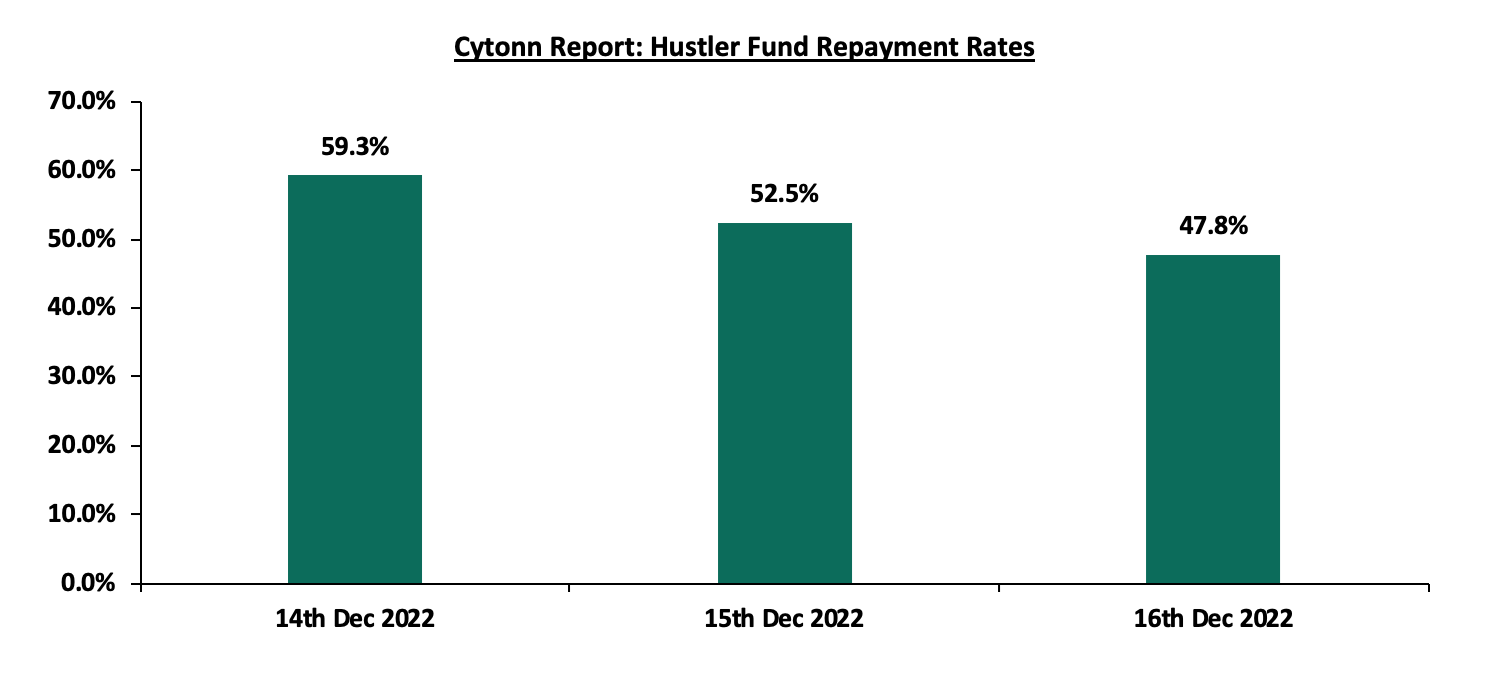

Further, the chart below shows the repayment rates as provided by the Co-operatives and MSME Development Ministry;

Source: Co-operatives and MSME Dev. Ministry

The objective of the Hustler Fund is to be a revolving fund hence the need to ensure its long-term sustainability. As such, we shall analyze the sustainability of the funds based on the following metrics;

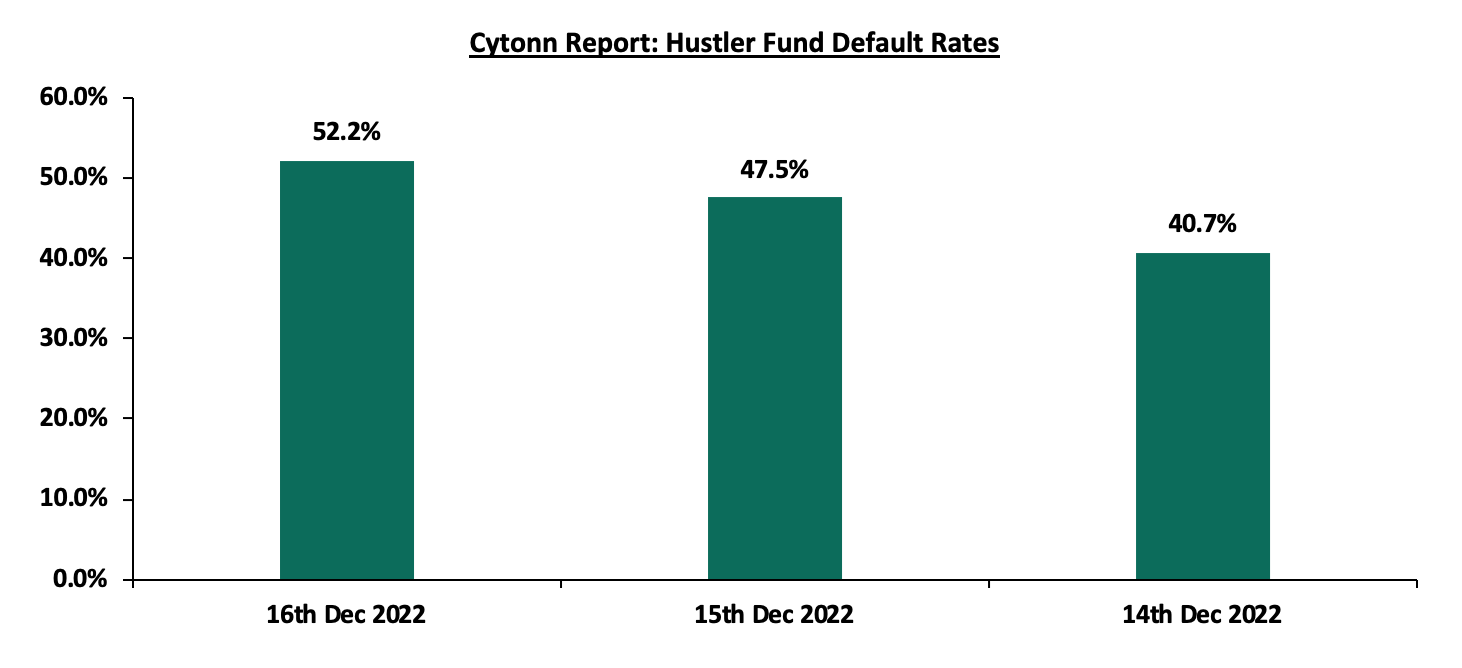

- Cost of Bad Loans – One of the major stumbling blocks affecting sustainability of Affirmative Action Funds is the high default rate. Based on the provided data on the performance of the fund, the average default rate is currently at 46.8%. This indicates that averagely, for every Kshs 100 lent out, Kshs 46.8 has been lost through bad loans. The chart below shows the default rates as provided by the Co-operatives and MSME Development Ministry;

Sources: Co-operatives and MSME Dev. Ministry

- Cost of Operations – The fund has set the cost of operations at 3.0% of the approved budget for a financial year indicating that for every Kshs 100.0 lent out, Kshs 3.0 will be used to cover for administration cost and various operations, and,

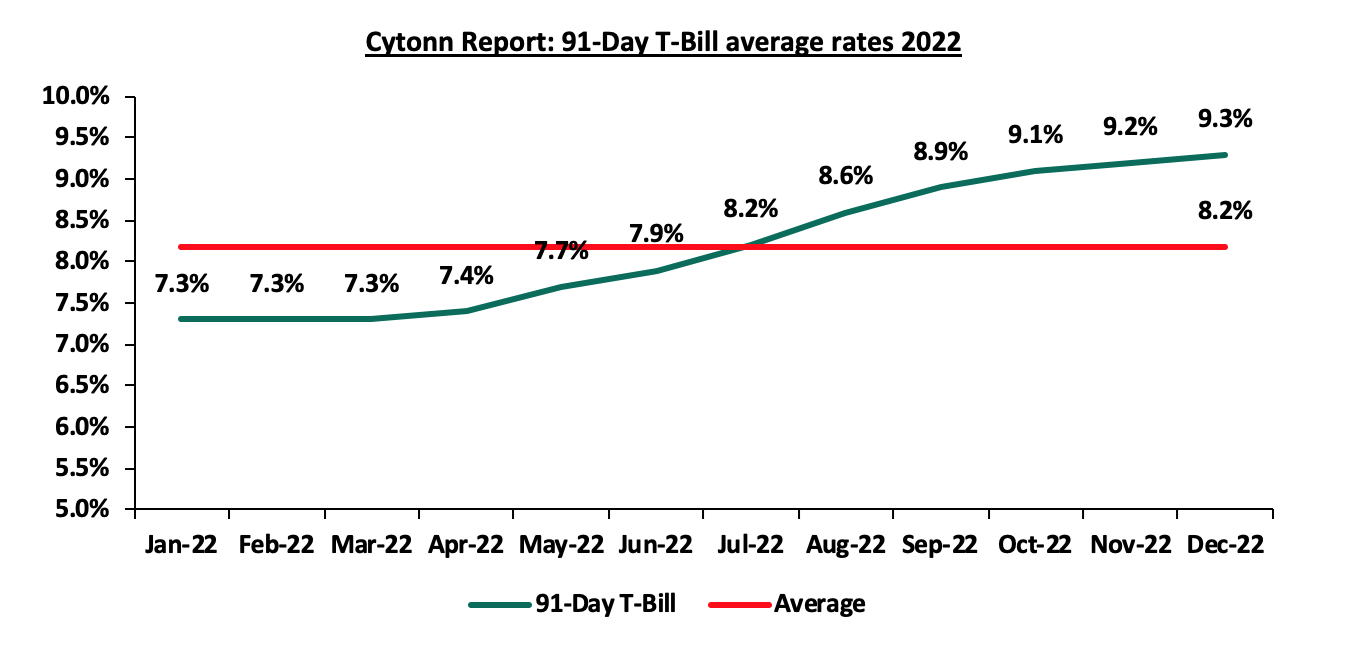

- Cost of Money – The cost of money refers to the expense that the government will incur when sourcing for funds. With Kenya already having a projected fiscal deficit of 6.2% of GDP in FY’2022/2023, it implies that financing the Hustler Fund is largely going to be financed through borrowing. Currently, the cost of short-term borrowing for the government, when using 91-day T-bill average is 8.2% for the year 2022. This indicates that for every Kshs 100.0 lent out, the government will use an estimated Kshs 8.2 to source for funds. The chart below shows the 91-day T-Bill rates for 2022;

Source: CBK

Key to note, summing up 46.8% for cost of bad loans, 3.0% for cost of operations and 8.2% for cost of money brings the cost of fund to 58.0%. This indicates that the government is lending out money at a cost of 58.0% compared to the interest rate of 8.0% charged on the fund. The table below highlights the cost of funding for the fund;

|

Cytonn Report: Hustler Fund Cost of Funds |

|

|

Cost of Bad loans |

46.8% |

|

Cost of Operations |

3.0% |

|

Cost of Money |

8.2% |

|

Cost of Funds |

58.0% |

|

Less the Interest Rate |

8.0% |

|

Net Loss |

50.0% |

As such, the government will probably have a net loss of 50.0% meaning that out of the Kshs 50.0 bn lent out, the government’s cost of funds will stand at Kshs 25.0 bn. From the analysis, the Hustler Fund appears unsustainable as it currently stands unless the government minimizes the potential risk of bad loans arising from high default rate for the sustainability of the fund.

Section 6: Conclusions and Recommendations

Based on the foregoing, we make the following conclusions.

- It’s a Great Initiative: The Hustler Fund is a good initiative because it attempts to address a key National Issue, access to credit is lacking and credit is expensive.

- Impact Remains Questionable: However, the Kshs. 50 billion has minor impact compared to the action problem which is a Kshs. 8.7 trilion of credit deficit required to reach 100.0% credit to GDP. The Hustler Fund addressed at best 0.6% of the problem before considering default rates.

- The Sustainability Remains Questionable: It appear the funds is set to lost about 50.0% of value mainly through default rates and costs of funds as discussed above, making it unsustainable unless the state decides to refinance the defaults on an annual basis.

Given above conclusions, we make the following recommendations both to address the issue of access to credit and the challenges to the fund;

- Stimulate Capital Markets to Contribute to Credit Markets – The most impactful action the government can take to address access to credit is to stimulate capital markets. The capital market in Kenya is under-developed as it contributes about 1.0% of total funding to businesses while the banking sector is already maxed out contributing 99.0% of funding. Key to note, the Kshs 50.0 bn fund, even if fully disbursed will only address 0.6% of the Kshs. 8.7 trillion credit deficit, hence it’s largely minimal because of the huge funding gap. Ideally, of the 12.1 tn credit to private sector that is needed to achieve Kshs. 12.1 tn credit to private sector, it should be a third from banking markets – roughly 4.0 tn; a second third from regulated capital markets – roughly 4.0 tn, and a final third – roughly 4.0 tn from private / alternative capital markets. With the current Kshs 3.6 tn coming from banking markets, the banking sector has essentially made its contribution leaving the capital markets to come in. As such, improving the capital markets framework is left as the only primary financing avenue that businesses can tap into. It is, thus, prudent for the government, in conjunction, with the financial sector regulators to develop a sound legal framework to promote transparency of the corporate bond market bonds, as well as investor education on key legislations that apply to the specific bond market,

- Sustainability –The fund’s model is likely to fail because of the low lending interest rates, coupled with higher cost of bad loans, cost of operations and cost of money. To ensure long-term sustainability, the fund should develop partnerships and collaborations with other public sectors and NGOs and use their competency, financial capacity and established networks to meet the objectives of the fund at cost-effective rates, and,

- Governance Framework – The government should ensure that the fund is professionally managed and free from political interference to ensure transparency and avoid mismanagement of funds which has been witnessed in the past. Any person found guilty of misappropriation of funds should be charged and prosecuted as spelt out in the draft regulations. The government can also set up an independent oversight body to ensure accountability at any point in time and ensure that the operations cost is maintained at a minimum level.